Don't sell your stocks based on what you read in the news!

Nearly every aspect of financial planning entails a level of uncertainty and change.

That is why it is critically important to make decisions based on strong historical evidence and thorough research.

In this article we're going to talk about why you should not change your portfolio based on what you see or read in the news.

Forgive me, but I'm going to start with some facts...

Between:

Feb 19th, 2020

23 trading days

March 23, 2020

The S&P 500 lost 35%

The fastest collapse on record.

Source: S&P

The next 51 trading days:

March 24th, 2020

51 trading days

June 8th, 2020

The S&P 500 gained 44%

The fastest recovery on record.

Source: S&P

During this period, there was one day when more stocks were sold than any other day in the history of the stock market.

Can you guess what day that was?

March 23th, 2020

THE BOTTOM!

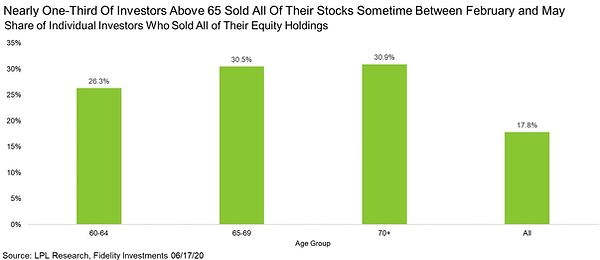

According to LPL & Fidelity investments, nearly one third of investors 65 or older sold all of their stocks between Feb 2020 and May 2020!

That means that they LOCKED IN up to a 35% loss!

It's important to remember that when the stock market plummets, you haven't lost any money. You've lost account value.

You lose money when you sell at a loss and lock in those losses.

Now, a 35% loss is bad enough but the deeper damage is the emotional damage that results from these decisions.

I've been a financial planner through two recessions. Here is what happens when you sell at a loss...

.png)

1) Selling based on fear can shift your investment mindset.

Instead of listening to historical results and rational advice, we shift our mindset to focus on fear and losses.

We all live with a certain amount of Confirmation Bias.

That is the tendancy to search for, interpret, favor or recall information that confirms or supports your beliefs.

Instead of believing the historical information about stock market returns, we instead search for answers that support our decisions.

-

"My stocks just dropped by 35%, but my savings gained money"

-

"It is going to take years for this economy to come back, my money is better in bonds or savings"

-

"See, the blah blah Times just posted that the death count increased from this virus, it's only going to get worse!"

Behavioral Psychology teaches us that we tend to feel the pain of a loss roughly twice as much as the joy of a gain.

As a result, any biases you may have to "protect" you from losses carry stronger emotional weight and are much harder to change.

Once you decide to act on fear, it becomes a much more difficult decision to reverse.

2) Selling based on fear introduces a whole new set of "variables" (decisions).

Making good financial choices is hard enough. What happens when you introduce a whole new set of decisions that need to be made to take action?

Think back to your original decisions to invest.

There are a number of barriers that prevent people from investing.

Because of this, it is likely that your financial planner, 401k administrator or robo-advisor has developed a system to remove these barriers.

This may be by:

-

Setting up a default (and automatic) target date investment fund.

-

Making investing as simple as defining your age and time horizon.

Now think of what happens after you make the decision to sell out of your investments based on the news.

Now that you've sold to cash, what is your next move?

What do you need to see to feel comfortable enough to invest back into the market?

-

Unemployment numbers?

-

GDP?

-

The S&P to reach XXXX points?

Inside perspective:

I have been a professional financial planner since 2007. I understand the importance of objectivity, discipline and rules based decisions.

During the deepest part of the Covid-19 pandemic selloff in March of 2020, I had deep struggles balancing my thoughts and my emotions when it came to my clients investment decisions.

Every "variable" you add to your investment process complicates your decision making which can lead to mistakes.

An oversimplification:

The boring stock market cliche's exist for a reason.

"Time IN the market is more important than timing the market."

"Buy Low Sell High" (selling after the market has lost value does not fit this)

According to the Motley Fool, the S&P 500 has ended the day POSITIVE over 70% of the time since 1950. I'll bet on those odds... 1

If you are ever considering making a change to your portfolio (10% shift or more) based on what you see in the news, I strongly urge you to first talk to any financial planner.

Talk to your retirement plan administrator.

Talk to any friend who you think is good with money.

Doing this can save you from making a mistake that can cost you a lot of money!

If you are interested in learning how to manage your investments, but don't know how to get started feel free to schedule a phone call. We're happy to help...

We're a different kind of financial firm than you may be used to.

1 - https://www.fool.com/investing/2019/05/14/6-stock-market-plunge-statistics-you-need-to-know.aspx

Disclaimer: The material and opinions provided in this document are meant for general illustration and/or informational purposes only and should not be construed as investment, tax, or legal advice for any individual. Although the information has been gathered from sources believed to be reliable, each reader must decide whether it is valid and applicable to his/her own unique circumstances. Any economic forecasts made in this commentary are merely opinion, and any referenced performance data is historical. As a result, neither is a guarantee of future results, as all investments involve risk.